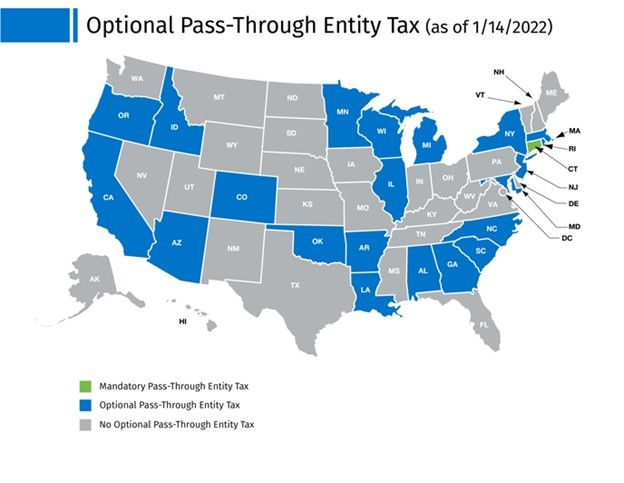

California passed AB150 for the tax years from 2021 – 2025 to provide workaround to the $10,000 federal cap placed on deducting state and local taxes (SALT). The elective PTE tax allow eligible pass – through entities (S – Corporation, Partnerships, and LLCs) to deduct state taxes at the entity level for federal tax purposes. There will be no deduction for California purposes. The shareholders, partners, or members will receive California tax credit equal to the PTE tax paid.

PTE election

An annual election is made on an original, timely filed tax return. Once the election is made, it is irrevocable for that year and is binding on all partners, shareholders, and members of the PTE.

PTE for 2022 to 2025 taxable years

Beginning on or after January 1, 2022, and before January 1, 2026, the election must be made when the tax return for the taxable year is filed, and the PTE must make an initial payment by June 15.

For questions and inquiries related to PTE tax, please contact our office at 310.666.0244

Reference:

https://www.ftb.ca.gov/file/business/credits/pass-through-entity-elective-tax/index.html

https://www.wolterskluwer.com/en/expert-insights/whole-ball-of-tax-elective-pass-through-entity-tax